EN

EN ES

ES DE

DE PL

PL IT

IT FR

FR GR

GR

Steady Market Confidence as Prices Drop Across Categories

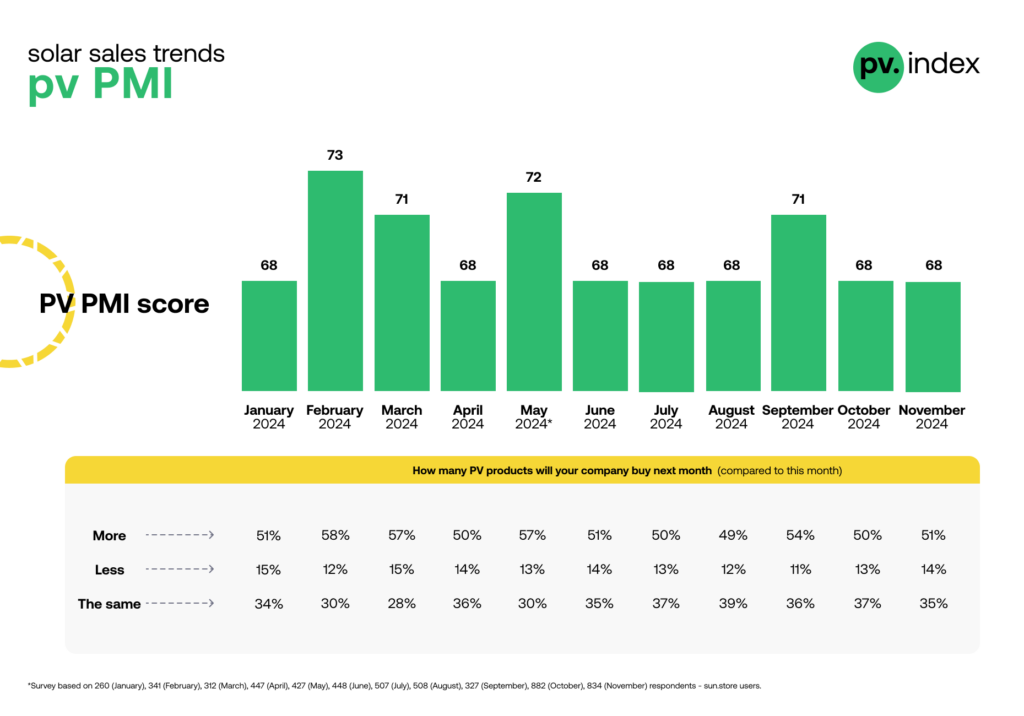

The European PV market remained steady in November, with the PV Purchasing Managers’ Index (PMI) holding firm at 68, consistent with October. While buyer confidence remains robust, solar component prices continued their downward trajectory across most categories, signaling a market grappling with seasonal adjustments and intensified competition.

Market sentiment and buyer behavior

The PV Purchasing Managers’ Index (PMI) remains a cornerstone for understanding market sentiment and demand trends in the European solar industry. This metric, derived from the purchasing intentions of over 20,000 registered users on the sun.store platform, serves as a valuable barometer of the industry’s health and future direction. With consistent participation from a diverse network of buyers—spanning installers, distributors, and many others—the PV PMI captures the nuanced shifts in purchasing behavior across the continent.

Sustained demand in a challenging market

In November, the PMI held steady at 68, maintaining the same level as in October. While this stability suggests resilience in demand, it also reflects a market that is cautiously navigating seasonal transitions and broader economic uncertainties. Buyers appear to be adjusting their strategies as the year-end approaches, with 51% planning to increase their purchases, a slight uptick from 50% last month. Meanwhile, 35% intend to maintain their current buying levels, and only 14% anticipate reducing their orders.

This balance indicates that the European solar market continues to demonstrate robust confidence, even in the face of declining prices. The steady PMI underscores the ongoing commitment of buyers to secure high-quality components, leveraging favorable pricing trends to optimize their procurement strategies. As seasonal factors influence installation timelines and stock replenishment, the consistent PMI provides a reassuring signal that demand for solar solutions remains strong as the industry gears up for the coming year.

Filip Kierzkowski, Head of Partnerships & Trading, shared his perspective: “This steady PMI demonstrates the resilience of the European solar market, even as we enter the traditionally slower months. It’s encouraging to see consistent interest in high-quality components, despite external challenges.”

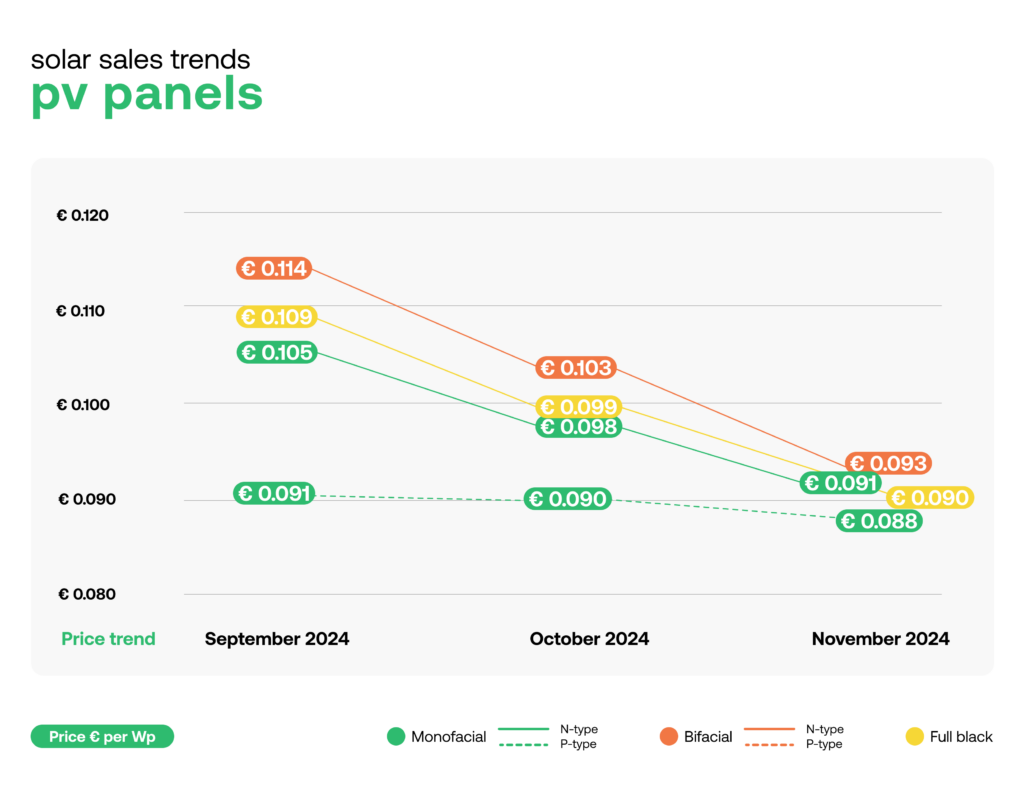

Key price trends for November: panels

Monofacial modules:

N-type: Prices fell by 7% to €0.091/Wp from €0.098/Wp in October. This decline reflects ongoing efforts by sellers to clear inventories ahead of year-end.

P-type: A more modest 2% drop brought prices to €0.088/Wp, down from €0.090/Wp, indicating relative stability in this category.

Bifacial modules:

N-type: Prices saw a significant 10% decline, reaching €0.093/Wp from €0.103/Wp, driven by intensified competition and surplus stock. P-type: Insufficient sample size to establish trends for this category.

Full black modules: Prices dropped by 9%, landing at €0.090/Wp, down from €0.099/Wp in October. The continued price decline highlights sustained oversupply and heightened competition among suppliers.

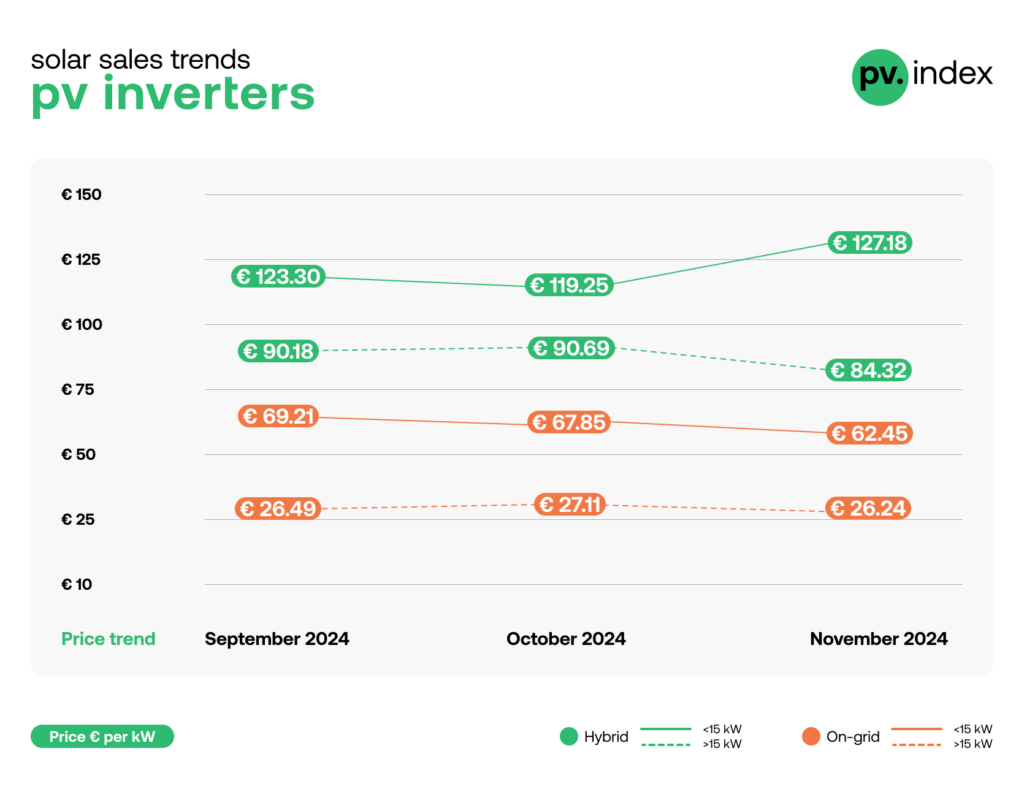

Inverter pricing: mixed movements

Hybrid inverters showing both increases and decreases depending on capacity, while on-grid inverters generally experienced declines across the board.

Hybrid Inverters:

<15kW: Prices rose by 7% to €127.18/kW, up from €119.25/kW in October. This uptick reflects increased demand for advanced residential solutions, particularly premium brands like Huawei.

15+ kW: Prices fell by 7% to €84.32/kW, down from €90.69/kW. Larger systems faced slower demand due to a shift in buyer focus toward smaller, more flexible installations.

On-grid Inverters:

<15kW: Prices dropped by 8%, reaching €62.45/kW compared to €67.85/kW in October. This decline is attributed to weaker residential demand as seasonal factors take hold.

15+ kW: Prices dipped by 3% to €26.24/kW, down from €27.11/kW, signaling stabilized demand in larger-scale projects.

Krzysztof Rejek, Head of Business Development at sun.store, offered insights into the trends:

“The downward pricing trend persisted in November, with all segments hitting new lows—some module offers even nearing €0.05/Wp. Distributors continue their stock liquidation strategies, driven by end-of-year warehouse clearance efforts.

Looking ahead to December, we anticipate a slight uptick in prices due to China’s limited production capacity and a reduction in export tax rebates for modules. However, the availability of discounted stock from distressed distributors is likely to keep the overall average prices at competitive levels.”

Brand preferences: Jinko and Solis dominate

Jinko Solar continued to lead across all panel categories—maintaining its position as the top choice among sun.store users. For inverters, Solis remained the preferred brand for systems under 15kW, while Huawei held its dominance in the 15+ kW category, reflecting their strong reputation for reliability and performance in larger installations.

In summary

The November pv.index paints a clear picture of a market marked by steady demand and competitive pricing. Panel prices continue to trend downward, while inverter categories present a mixed bag of price changes influenced by evolving buyer preferences and year-end dynamics.

As sun.store crosses 20,000 registered users and remains the largest solar marketplace in Europe, the pv.index continues to be an indispensable resource, providing unparalleled insights for buyers and sellers navigating the ever-changing solar landscape.

About – pv.index & The PV Purchasing Managers’ Index (PV PMI)

pv.index traces current trading prices for solar components on a monthly basis. Data is recorded on sun.store, the biggest online PV trading platform with 7.8 GW+ of components on offer. Trading prices are weighted by the power of components involved in the transactions to arrive at a reliable estimate for the whole market.

The PV Purchasing Managers’ Index (PV PMI) is a measure indicating the overall sentiment towards the demand in the PV industry. PV PMI shows whether demand is expected to expand (above 50), remain stable, or contract (below 50), as perceived by purchasing managers.

The PV PMI was calculated as: PMI = (P1 * 1) + (P2 * 0.5) + (P3 * 0), where: P1 = percentage of answers reporting an improvement, P2 = percentage of answers reporting no change, P3 = percentage of answers reporting a deterioration. Survey is based on a sample of 800+ sun.store buyers.