EN

EN ES

ES DE

DE PL

PL IT

IT FR

FR GR

GR

Stability persists as stock levels tighten in March 2025

March painted a picture of cautious stability in the European solar market, with module prices showing minimal movement and inverter prices continuing to soften. However, beneath this calm surface, stock levels are dwindling across Europe, leaving installers and EPCs scrambling to secure specific module types – particularly for commercial and industrial (C&I) and small utility projects. Meanwhile, the PV Purchasing Managers’ Index (PMI) dipped slightly to 70, still reflecting strong buyer confidence as the industry navigates tightening supply and selective opportunities.

Despite the overall stabilization, great deals remain available – especially for full black modules and stock older than 6 months. sun.store continues to offer attractive pricing, though such bargains are becoming harder to find as availability shrinks.

The PV Purchasing Managers’ Index (PMI) continues to serve as a vital tool for evaluating market mood and demand shifts within Europe’s solar sector. Compiled from the buying plans of over 600 participants, drawn from a community exceeding 25,500 sun.store registrants, this index provides a clear picture of the industry’s present state and its likely path forward. By tapping into the perspectives of a varied mix of installers, distributors, and other stakeholders, the PV PMI sheds light on evolving procurement behaviors, offering valuable clues about significant trends shaping the solar market across the region.

PV PMI: Confidence holds steady at 70

March’s PV PMI settled at 70, a slight decline from February’s 73, yet still signaling robust optimism among buyers. Based on responses from 627 users out of over 25,500 registered on the sun.store platform, the survey showed:

- 53% plan to increase purchases, indicating proactive procurement amid tightening stocks.

- 35% intend to maintain current order volumes, reinforcing a stable market baseline.

- 12% foresee a reduction, a consistent minority reflecting selective caution.

Calculated as PMI = (P1 * 1) + (P2 * 0.5) + (P3 * 0)—where P1 is improvement, P2 no change, and P3 deterioration—this score highlights a market adapting to supply challenges while preparing for an active spring.

Key Drivers:

- Dwindling stock levels:

Inventories across Europe are shrinking, particularly for modules suited to C&I and small utility projects, pushing buyers to act swiftly.

- Selective opportunities

Very attractive deals on older stock (6-18 months) and full black modules persist, though they’re increasingly scarce.

- Spring momentum

With installation season underway, confidence remains high despite logistical hurdles.

Expert commentary: The market in transition

Filip Kierzkowski, Head of Partnerships and Trading at sun.store, noted:

“March reveals a market in transition. The PMI of 70 shows buyers are still confident, but stock shortages are posing real hurdles – particularly for installers and EPCs seeking specific module types for C&I and small utility projects. While prices hold steady, the best deals, like those on full black or older stock, are disappearing quickly. Platforms like sun.store remain a lifeline for seizing these opportunities. We’re also seeing a gradual return of interest in pre-booking stock, a trend that’s picking up as clients look to secure supply ahead of time – something our platform makes possible.”

Krzysztof Rejek, VP of Sales at sun.store added:

“We’re seeing a bottleneck emerge as stock levels drop. Demand is there, but availability isn’t keeping pace, particularly in key segments. That said, savvy buyers can still find great value – think modules from mid-2023 to late 2024 – though they’ll need to move quickly.”

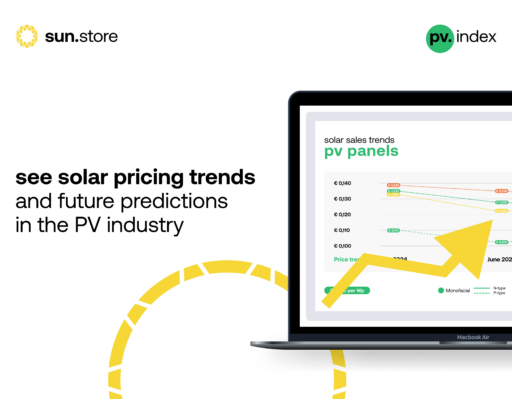

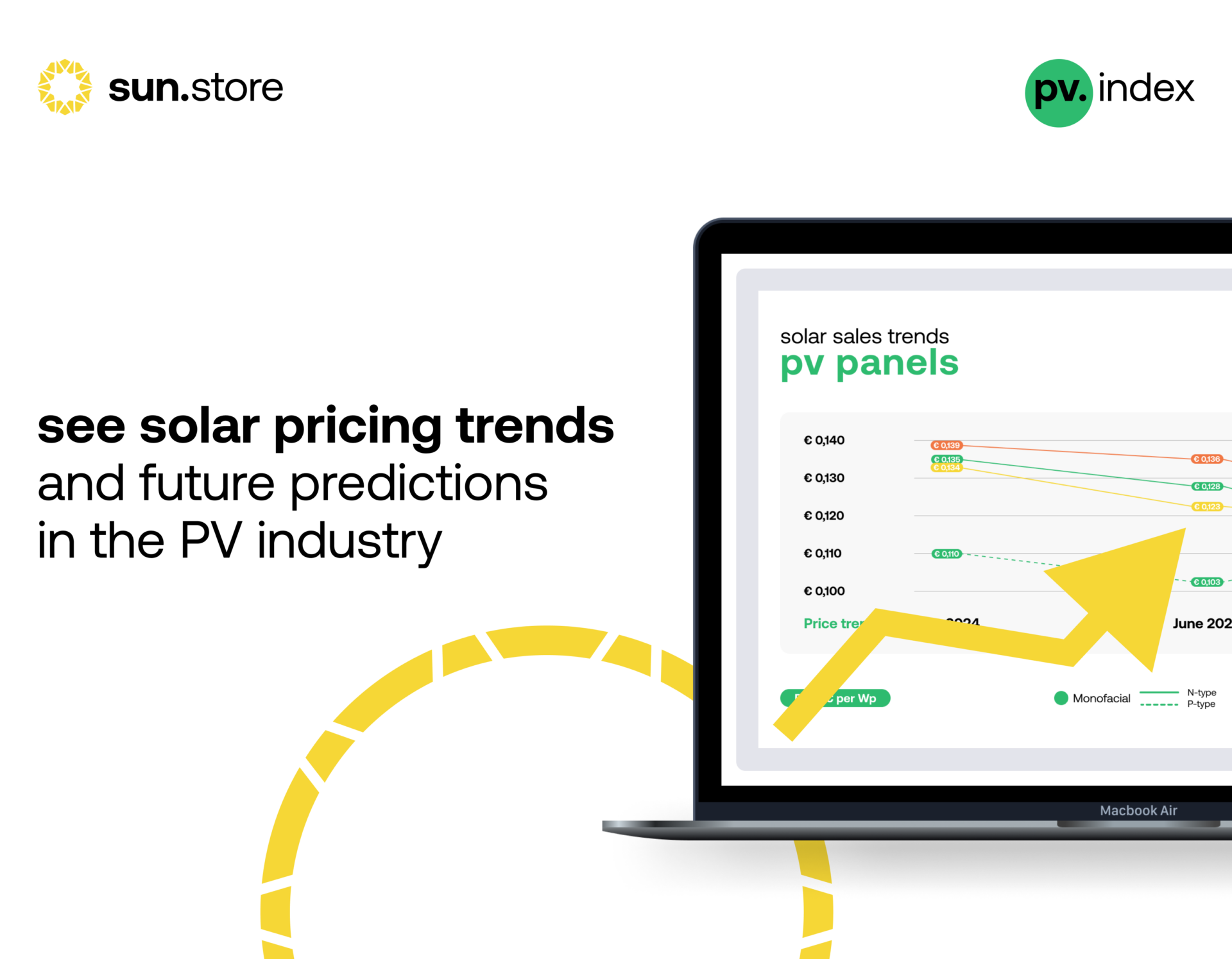

Module prices: Stability with pockets of opportunity

March module prices held steady across most categories, though stock constraints and selective discounts shaped the landscape:

Monofacial modules:

N-type: Prices remained at €0.100/Wp (0% change), reflecting a balance between demand and tightening supply for high-efficiency options.

P-type: Prices edged down to €0.077/Wp, a 1% drop, as standard modules face softer demand amid a shift to premium alternatives.

Bifacial modules:

N-type: Prices stayed at €0.094/Wp (0% change), with steady interest in bifacial technology for larger projects offset by limited stock growth.

P-type: Insufficient sample size to establish trends.

Full black modules:

Prices fell to €0.093/Wp, a 3% decline, proving that good deals still exist despite broader stabilization. Limited availability drove this discount, and platforms like sun.store remain key for securing such offers as stocks dwindle.

Across Europe, installers and EPCs are struggling to source the exact module types needed, especially for C&I and small utility installations. Meanwhile, older stock from 6-18 months ago offers very attractive pricing—a silver lining for those willing to adapt.

Inverter pricing: Declines reflect weaker demand

Inverter prices continued to soften in March, driven by weaker demand in residential and small C&I segments, alongside oversupply from certain brands:

Hybrid Inverters:

<15kW: Prices dropped to €114.84/kW, a 5% decrease, as residential demand eased and competition intensified among oversupplied brands. Distributors are working to clear excess stock, pushing prices lower.

>15kW: Prices held steady at €88.48/kW (0% change), suggesting a pause in the softening trend for larger hybrid systems.

On-grid Inverters:

<15kW: Prices fell to €53.93/kW, a 3% reduction, reflecting weaker residential uptake and persistent supplier pressure to move inventory..

>15kW: Prices dipped to €24.34/kW, down 2%, as large-scale segment competition and oversupply from select brands kept downward momentum alive.

Certain manufacturers remain heavily oversupplied, leaving distributors scrambling to reduce stocks – a dynamic keeping inverter prices attractive for buyers.

Brand preferences: Jinko and Huawei take the lead

March data showcased shifting brand loyalty:

Modules: Jinko reclaimed the top spot, favored for its reliability and availability across monofacial and bifacial lines.

Inverters:

<15kW: Huawei surged ahead, dominating the residential and small C&I market with competitive offerings.

>15kW: Huawei also led, cementing its strength in larger installations.

These preferences highlight a focus on proven performance amid supply constraints.

Outlook for the coming months

With a PMI of 70 and stock levels tightening, the European solar market is at a crossroads. Module prices remain stable, but availability issues – especially for C&I and small utility projects – could intensify. Inverters, meanwhile, benefit from softer demand and oversupply, keeping prices low.

Buyers can still find great deals, like the full black discount or older stock on sun.store, but these opportunities are fading fast. As spring unfolds, the market’s ability to balance supply and demand will shape Q2’s trajectory.