EN

EN ES

ES DE

DE PL

PL IT

IT FR

FR GR

GR

September 2025: Premium battery prices stabilize, performance batteries edge lower, and commercial demand remains steady

sun.store releases the third edition of its Battery Index – a monthly report tracking energy storage pricing and brand dynamics across Europe. Drawing on real transactional data from Europe’s largest PV and storage marketplace, the Battery Index provides installers, distributors, and EPCs with reliable benchmarks and a clear perspective on how the market continues to evolve.

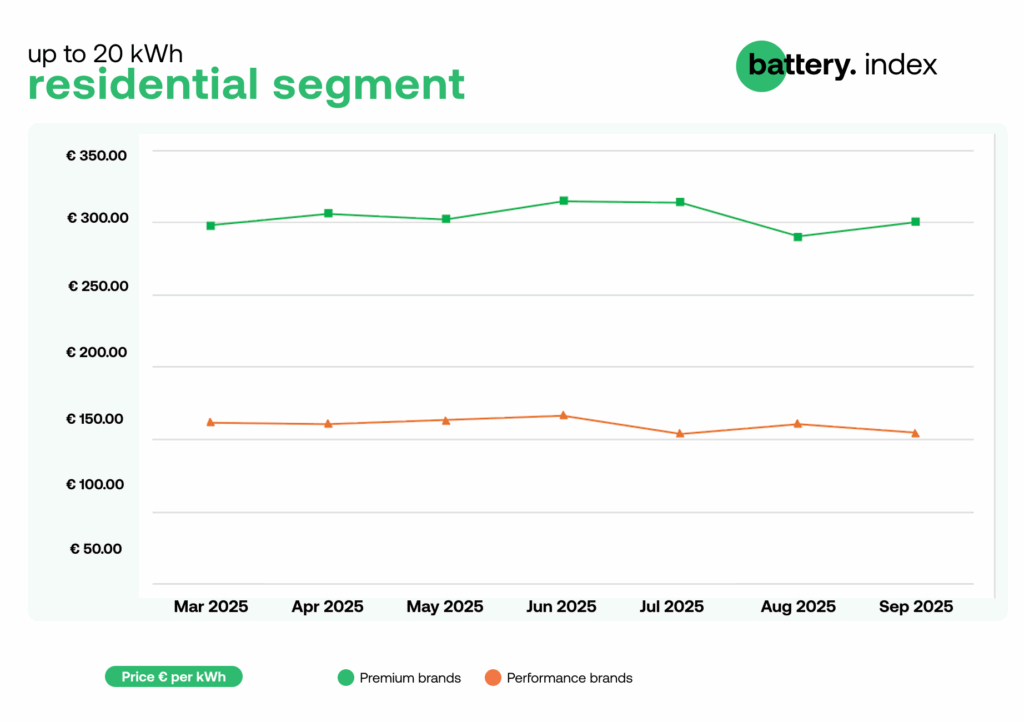

Residential segment (up to 20 kWh): premium battery prices stabilize, performance softens

The residential battery market entered calmer waters in September. Average prices for premium brands remained largely stable, holding close to €300/kWh, signaling that the earlier downward correction has paused as inventories normalize and supply chains regain balance.

Meanwhile, performance-oriented batteries experienced a modest decline – slipping from around €159/kWh in August to roughly €150/kWh in September. This downward movement reflects easing component costs and stronger competition among mid-range suppliers, as distributors clear stock ahead of Q4 procurement cycles.The result is a slightly widened price gap between premium and performance segments – reversing the narrowing trend observed in August, yet still remaining around the 100% mark, confirming the lasting structural divide between both tiers of the market.

“In September, premium battery prices held steady while performance models saw a modest decline. The widening price gap between both segments suggests that installers remain willing to pay a substantial premium for recognized brands, reflecting sustained demand in the upper tier rather than an overall market correction.” – comments Grzegorz Furman, International Senior PV Trader.

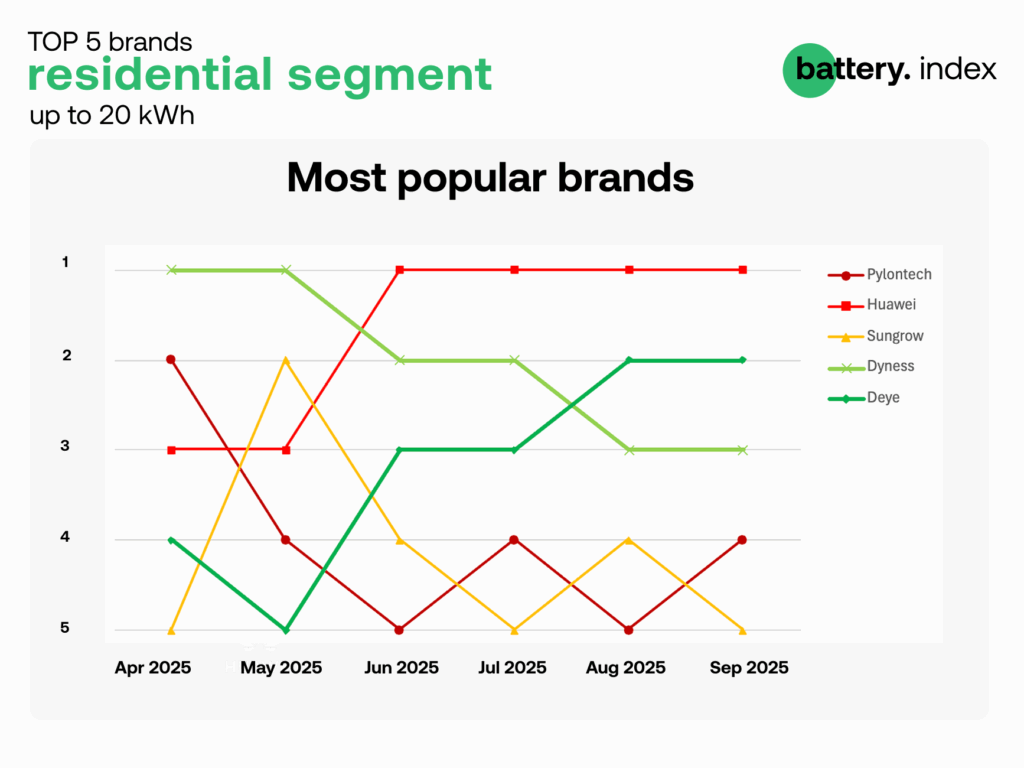

Top 5 battery brands: September 2025

The residential Top 5 saw few notable changes in September. Huawei maintained its firm leadership for the fourth consecutive month, while Deye strengthened its position as the main challenger. Dyness continued to lose ground, dropping further behind the two leaders due to softening demand and reduced availability, whereas Sungrow and Pylontech traded places – Pylontech returning to the Top 5 after a brief dip in August.Overall, Huawei and Deye dominate the premium and performance categories respectively, shaping installer preferences across Europe’s residential segment.

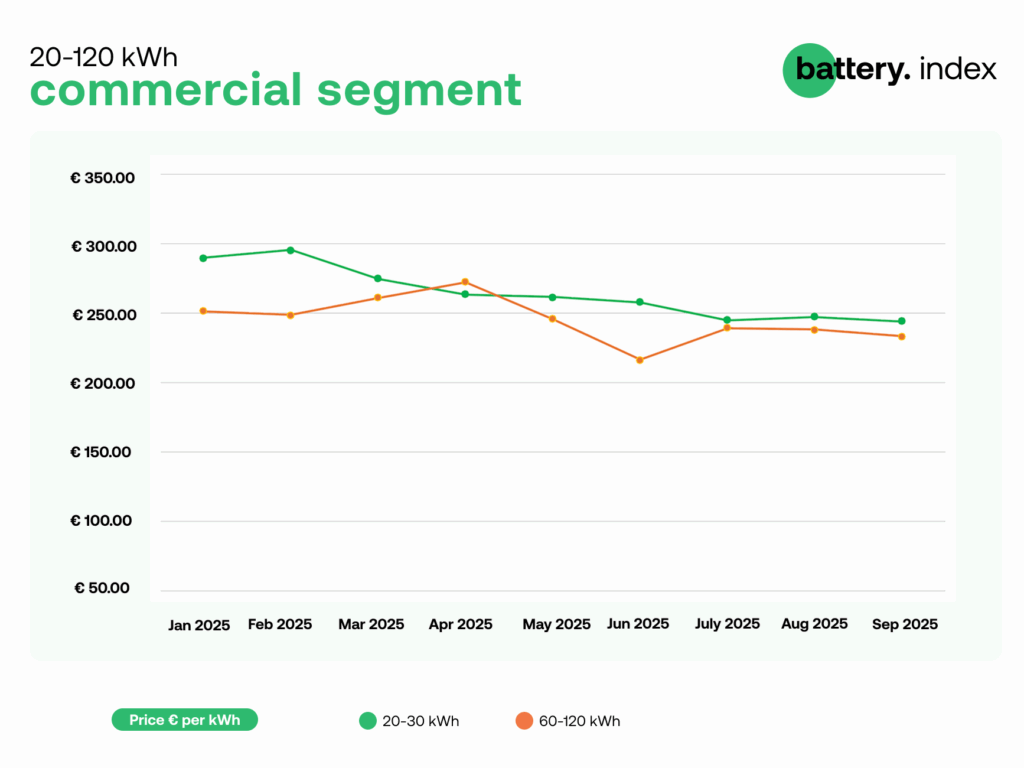

Commercial segment (20-120 kWh): steady trajectory

Price movements in the commercial segment remained moderate throughout September. Systems in the 20–30 kWh range averaged around €245/kWh, virtually unchanged from August, while the 60–120 kWh segment recorded a slight dip from roughly €238/kWh to €232/kWh.This continued stability underscores how commercial buyers operate on longer planning cycles, where quarterly rather than monthly adjustments dominate pricing. As project pipelines remain consistent, the market for medium and large-scale storage solutions continues to show resilience despite seasonal slowdowns.

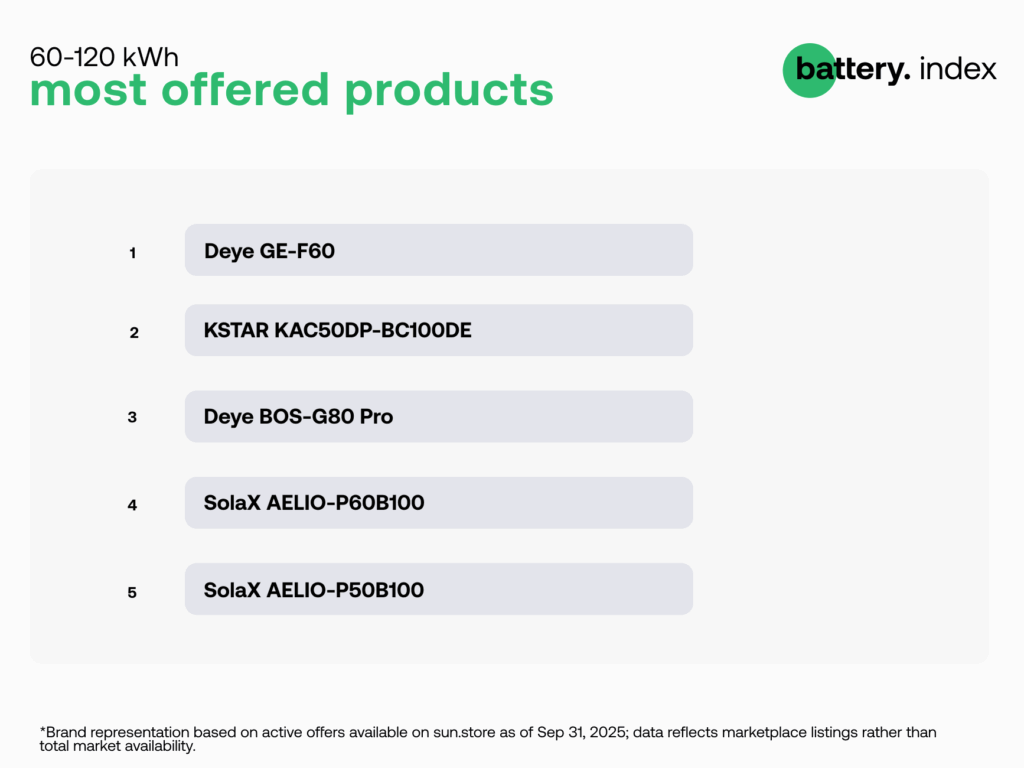

Most offered products

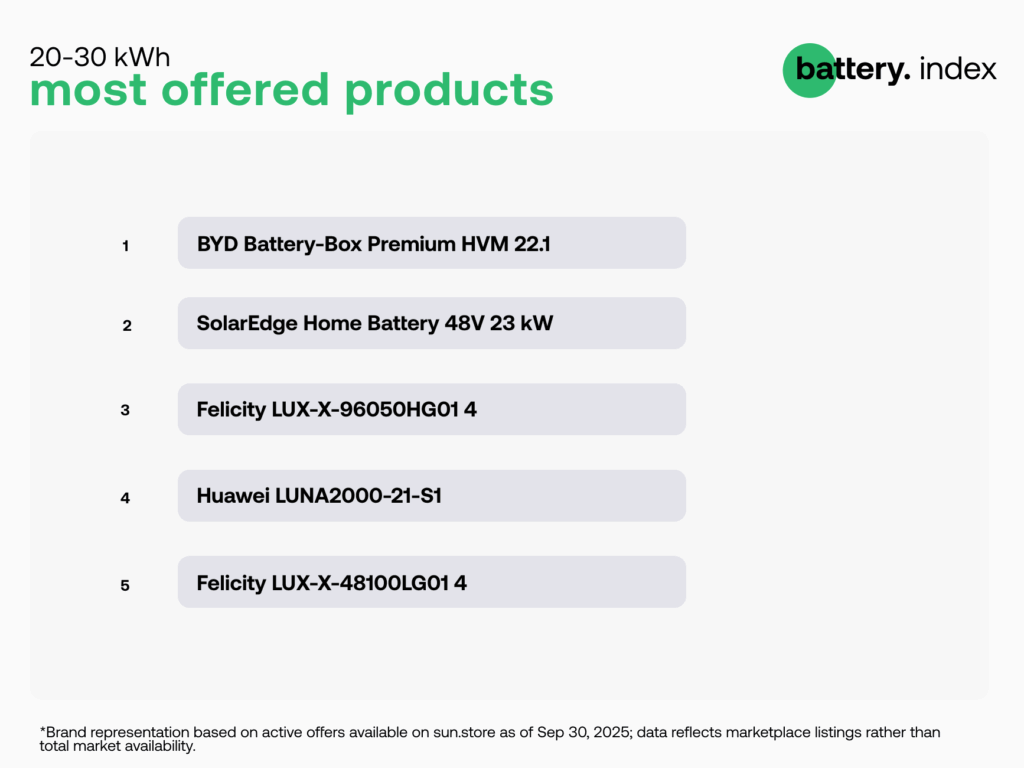

20–30 kWh segment

- BYD Battery-Box Premium HVM 22.1

- SolarEdge Home Battery 48V 23 kW

- Felicity LUX-X-96050HG01 4

- Huawei LUNA2000-21-S1

- Felicity LUX-X-48100LG01 4

The 20–30 kWh range remains a diverse testing ground for installers and distributors, mixing established premium names such as BYD and Huawei with emerging mid-range brands like Felicity.

60–120 kWh segment

- Deye GE-F60

- KSTAR KAC50DP-BC100DE

- Deye BOS-G80 Pro

- SolaX AELIO-P60B100

- SolaX AELIO-P50B100

The upper commercial range continues to be dominated by Deye and KSTAR, highlighting their strong foothold in the C&I segment. SolaX maintains visibility with two models in the Top 5, illustrating its competitive presence in higher-capacity offerings.