EN

EN ES

ES DE

DE PL

PL IT

IT FR

FR GR

GR

Market steadies as inverter prices tick up and Jinko reclaims the lead

The European PV market entered October in a phase of clear stabilization. After months of gradual price declines, most product categories showed flat or slightly positive movements, signaling that the market may have reached its floor. The pv.index PMI remained unchanged at 66, reflecting steady sentiment among installers and distributors heading into the final months of the year.

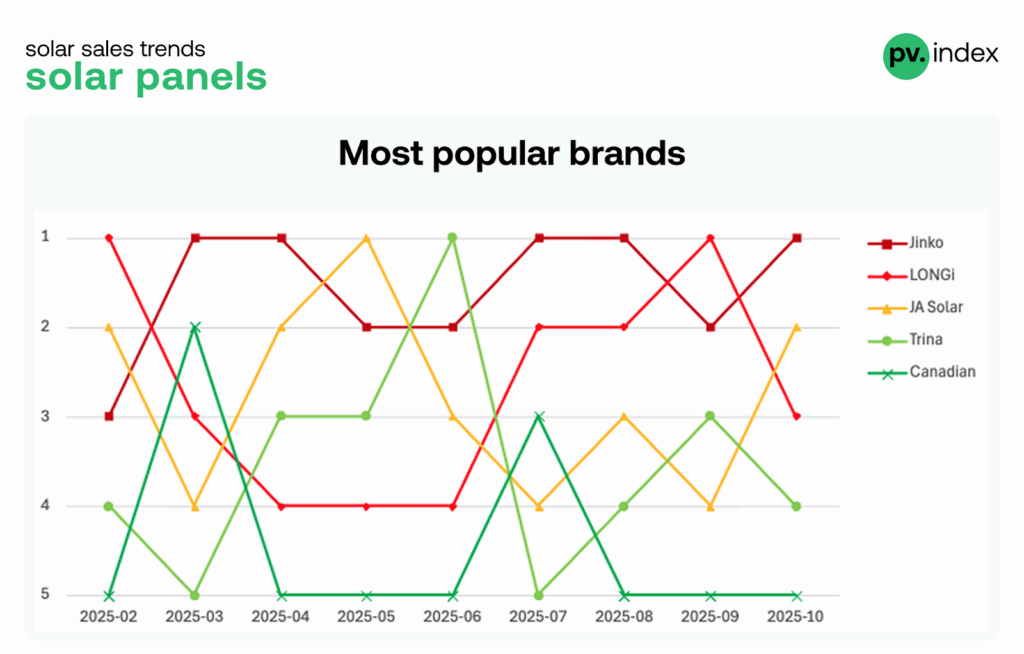

The main highlight of this edition is a reshuffle in the solar module ranking, with Jinko Solar returning to the top position and JA Solar advancing to second place, pushing LONGi down to third.

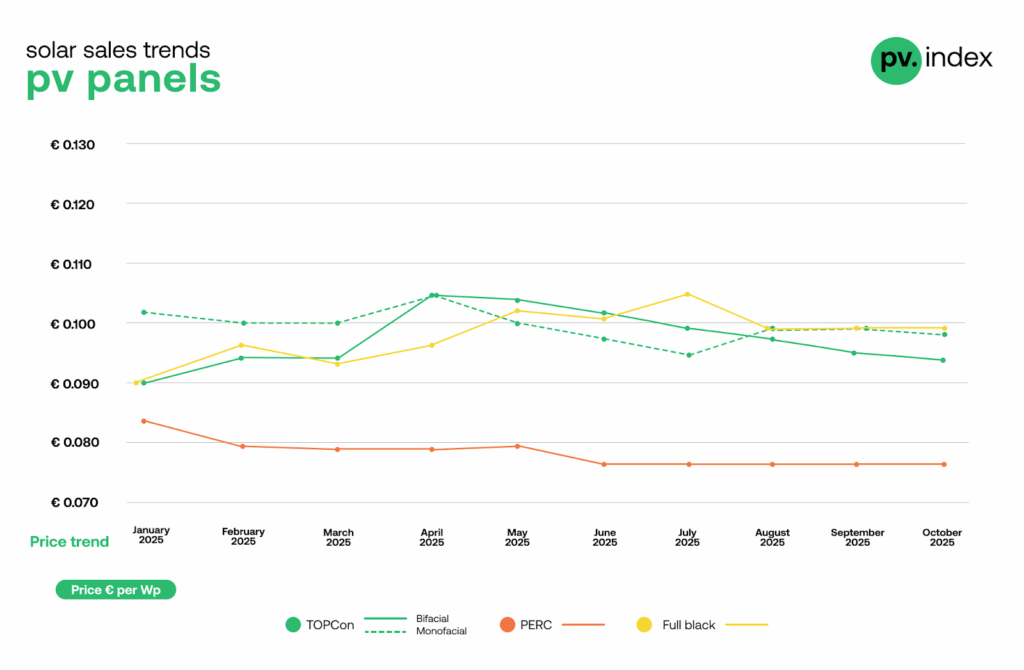

Solar module market: prices stabilize at the bottom

The European PV module market continues to display low volatility, reflecting a period of sustained equilibrium between production and demand. Over recent months, prices across all major technologies have remained largely steady, with only minor downward adjustments observed in specific categories. October data confirm that the market has now settled into a stable pattern, supported by balanced supply conditions and consistent purchasing activity from installers.

TOPCon modules continued a modest downward correction:

- Bifacial: €0.094/Wp, –2% month-on-month

- Monofacial: €0.098/Wp, –1%

PERC modules remained flat at €0.077/Wp, marking the fourth consecutive month without significant movement.

Full Black modules held steady for the third month in a row at €0.099/Wp, supported by strong residential demand and aesthetic appeal.

This stabilization reflects a healthy balance between supply and demand. Channel inventories are now better aligned with installation activity, and distributors report smoother turnover with fewer aggressive discounts.

Changing of the guard: Jinko leads, JA Solar ascends

Jinko’s return to the top confirms its regained supply strength and pricing competitiveness, while JA Solar’s climb to second place highlights its growing traction in European markets. LONGi, once dominant, faces increased competition from brands leveraging flexible distribution and aggressive pricing strategies.

Top 5 solar panel brands – October 2025

- Jinko Solar

- JA Solar

- LONGi

- Trina

- Canadian Solar

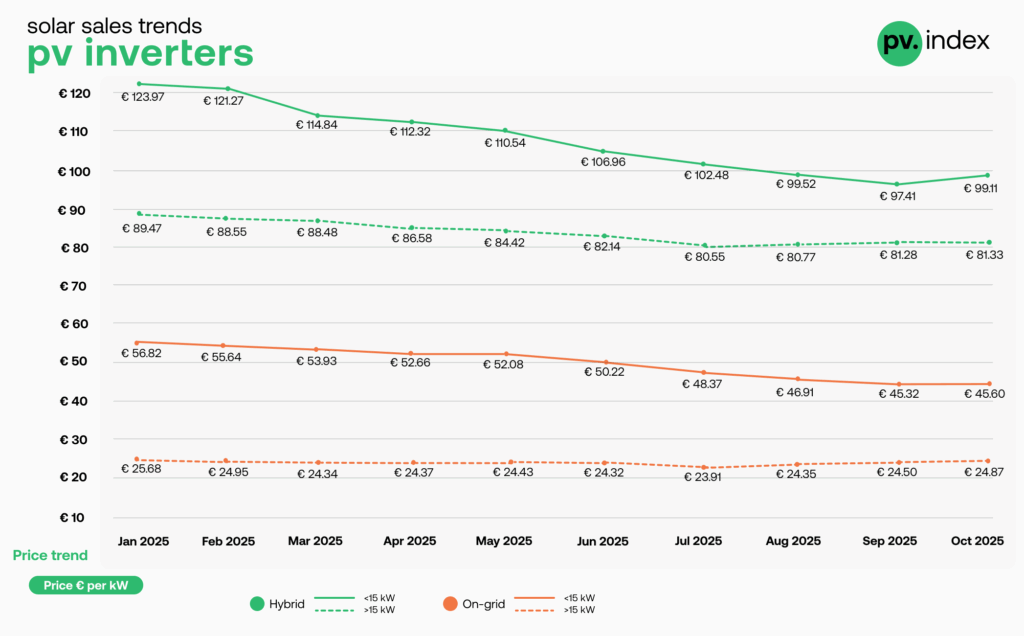

Inverter market: first positive movement in months

For the first time since spring, inverter prices showed a mild upward correction, signaling that the price adjustment phase may have reached its end. Stable component supply and stronger autumn demand supported a more balanced pricing environment across both hybrid and string segments.

- Hybrid inverters

- <15 kW: up 2% to €99.11/kW, marking the first increase since April. The rise was driven by steady residential demand and seasonal restocking by installers preparing for winter installations.

- >15 kW: flat at €81.33/kW, reflecting continued stability in the commercial segment, where larger projects are benefiting from long-term procurement contracts and steady pipeline activity.

- <15 kW: up 2% to €99.11/kW, marking the first increase since April. The rise was driven by steady residential demand and seasonal restocking by installers preparing for winter installations.

- String inverters

- <15 kW: up 1% to €45.60/kW, ending a months-long decline. The uptick suggests the segment has reached its price floor as inventories normalize and distributors ease discounting pressure.

- >15 kW: up 2% to €24.87/kW, supported by stronger commercial project activity and modest demand recovery in southern Europe, where delayed summer installations are now being completed.

- <15 kW: up 1% to €45.60/kW, ending a months-long decline. The uptick suggests the segment has reached its price floor as inventories normalize and distributors ease discounting pressure.

Overall, the inverter segment appears to have stabilized ahead of winter, with balanced stock levels and renewed buyer confidence after an extended correction phase.

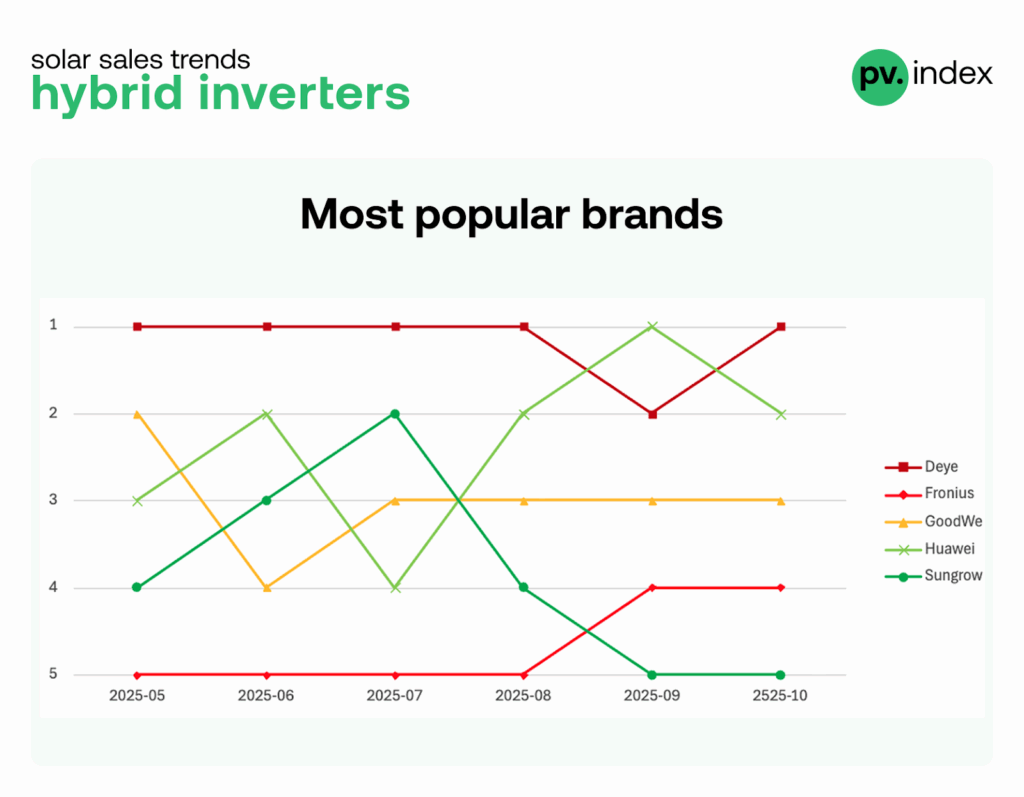

Huawei extends dominance as Deye returns to the hybrid lead

After several months of gradual price normalization, the inverter segment saw renewed activity in October – and subtle but notable shifts in brand rankings. Both hybrid and string categories reflect a market that is stabilizing yet still competitive at the top.

Hybrid inverters: Deye back in first place

Following a brief dip to second place in September, Deye has reclaimed the No. 1 position in the hybrid inverter ranking. The brand’s strong European distribution channels and attractive price-performance ratio helped it regain momentum heading into Q4. Huawei now moves to second, maintaining close competition thanks to its expanding hybrid portfolio and strong demand from premium residential installers. GoodWe remains steady in third place, supported by consistent supply and reliability in mid-range projects. Fronius and Sungrow complete the Top 5 with stable performance and broad market coverage.

Top 5 hybrid inverter brands: October 2025

- Deye

- Huawei

- GoodWe

- Fronius

- Sungrow

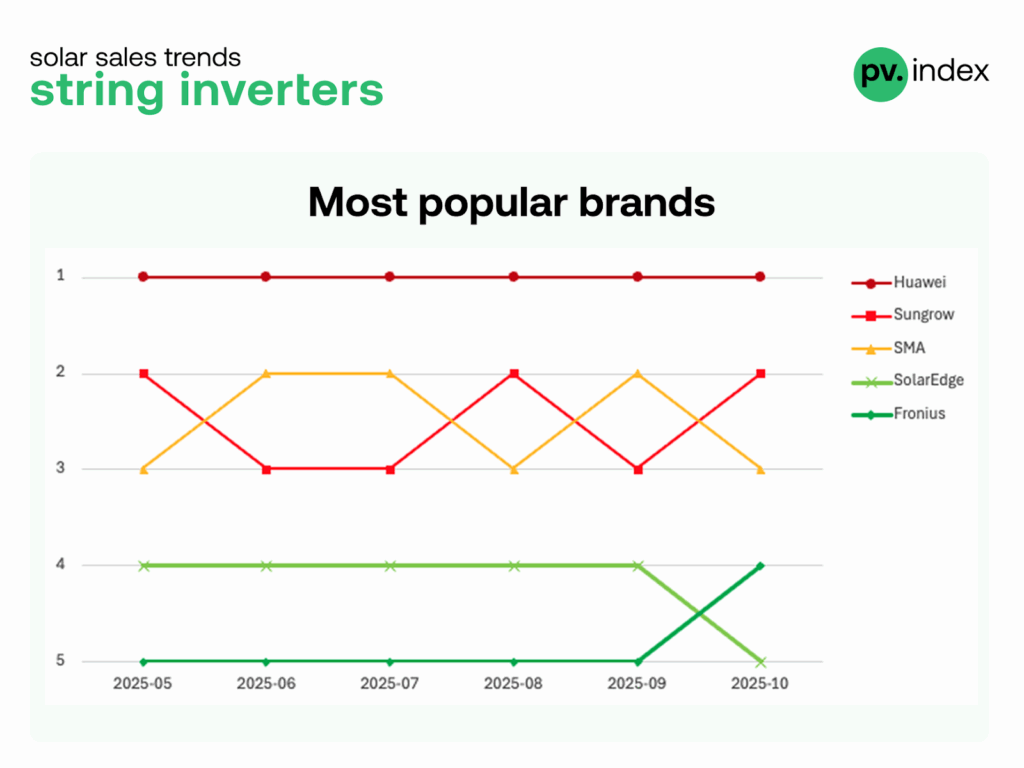

String inverters: Huawei leads unchallenged, Fronius climbs to fourth

In the string inverter category, Huawei continues its unbroken leadership streak – maintaining the top spot throughout 2025 and widening its gap to competitors. The real action took place just below: Sungrow and SMA once again traded places in positions two and three, continuing their close rivalry across key European markets. The main change this month occurred further down the list – Fronius advanced to fourth place, overtaking SolarEdge, which now ranks fifth. The shift reflects improved availability and stronger channel activity for Fronius in Central Europe, where installers increasingly value local support and service continuity.

Top 5 string inverter brands: October 2025

- Huawei

- Sungrow

- SMA

- Fronius

- SolarEdge

October’s ranking updates show that while Huawei’s dominance remains uncontested, other manufacturers are actively repositioning within a now-stable market. The renewed rise of Deye and Fronius underscores a broader shift toward reliability, regional support, and channel consistency as key differentiators heading into 2026.

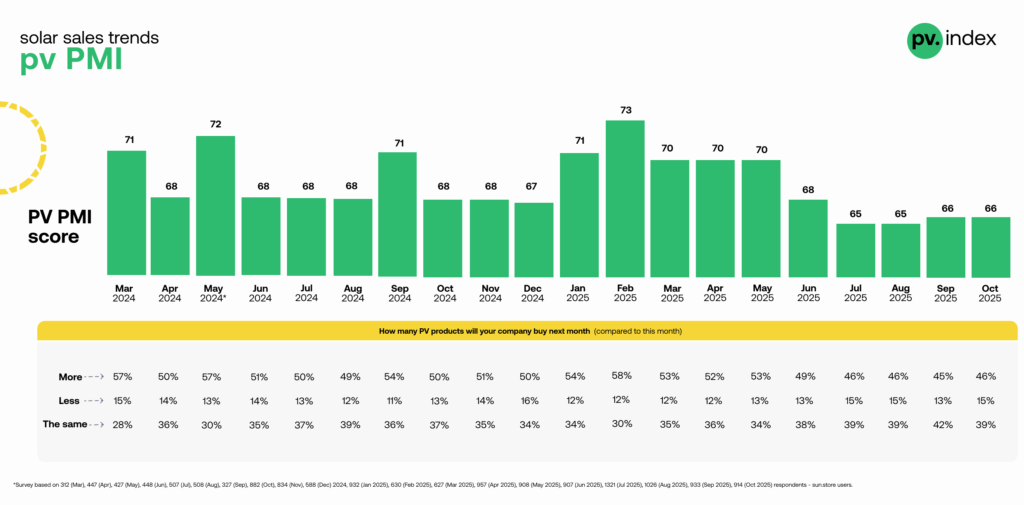

PV PMI sentiment remains stable

The pv.index PMI stood at 66 points in October, flat compared to September.

Survey data from 914 sun.store users show:

- 46% expect to buy more PV products next month

- 15% expect to buy less

- 39% expect no change

This stability suggests that distributors are keeping a cautious yet consistent purchasing rhythm as the installation season winds down. Market participants increasingly prioritize predictability and stock optimization over speculative buying.

*Calculated as PMI = (P1 x 1) + (P2 x 0.5) + (P3 x 0.5) — where P1 is improvement, P2 no change, and P3 deterioration. This score highlights a market adapting to supply constraints while gearing up for the peak installation season.

Expert commentary

“October confirms that the European PV market has reached equilibrium. Module prices have flattened across technologies, and inverter pricing has finally stabilized after months of decline” – says Filip Kierzkowski, Head of Partnerships & Trading at sun.store.

“What we’re seeing now is not a downturn, but normalization. The market has adapted to post-correction dynamics with a stable PMI, generally balanced inventories, and growing confidence heading into the winter months. However, for some manufacturers we are observing a noticeable increase in shipments to Europe, which could once again lead to temporary stock accumulation and intensified clearance activity — a scenario similar to what we saw late last year. Leadership consolidation among brands like Jinko, Huawei, and Deye shows that the sector is shifting from aggressive price competition toward long-term reliability and strategic stock management.”

Summary

October’s pv.index reflects a steady and balanced market.

- Prices: largely flat or slightly positive across categories

- Sentiment: stable PMI at 66 points

- Rankings: Jinko reclaims the top spot, Huawei and Deye maintain leadership

As 2025 nears its close, the European PV market appears firmly grounded. After a year defined by adjustment and recalibration, the sector is now positioned for a more predictable and sustainable start to 2026.

About – pv.index & The PV Purchasing Managers’ Index (PV PMI)

pv.index tracks monthly trading prices for solar components on sun.store, Europe’s largest B2B marketplace for PV equipment. Our pricing data is weighted by transaction power, providing a true market reflection.

Brand rankings are based on total sales value on sun.store between January and October 2025, identifying the most in-demand brands in each category. We update these rankings monthly to reflect current buyer preferences and market conditions.

The PV PMI gauges purchasing sentiment among verified sun.store users. It is calculated using the formula: PMI = (P1 × 1) + (P2 × 0.5) + (P3 × 0), where P1 = % expecting improvement, P2 = % expecting no change, and P3 = % expecting decline. A score above 50 signals a positive market outlook.